Often hailed as the “land of opportunity”, the US lived up to its reputation after becoming one of the first advanced economies to reach its pre pandemic level in Q2. Growth has now naturally begun to moderate, which will gain momentum in 2022 owing to a significant fiscal drag. Although Jerome Powell’s second term as Fed Chair has been all but confirmed, the policy outlook is somewhat uncertain given the emergence of Omicron. Meanwhile, the administration’s weak grip on Congress is set to slip further after the midterm elections, with Republicans likely to make gains in the House and the Senate.

Growth may have peaked, but the recovery still has legs

A combination of vaccinations and stimulus cheques saw the world’s largest economy unwind the COVID‑19 hit to GDP in Q2 with a robust 6.7% annualised expansion. But growth went on to wane to just 2.0% in Q3 owing to the spread of the Delta variant, supply chain disruption and fading fiscal support. Whilst monthly activity metrics point to a pick‑up in Q4, the general trend will be one of moderation through 2022 as the reining in of government support exerts a sizable fiscal drag. Partially offsetting this will be the gradual recovery in the service sector as consumer confidence is rebuilt and white‑collar workers return to the office in greater numbers, funded by a drawdown of accumulated savings and wealth. Following an expected 5.5% expansion this year, the Bloomberg consensus is for growth to moderate to 3.9% in 2022. However, this is threatened by the new Omicron strain.

If workers don’t return, the job market risks overheating

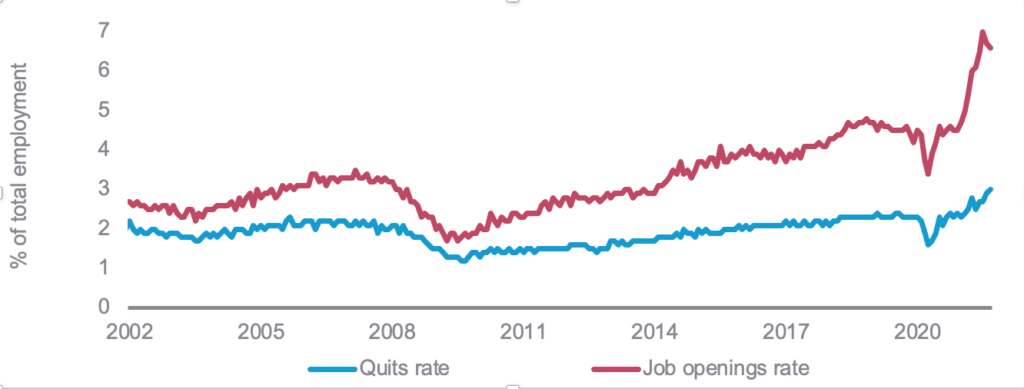

Amidst this rapid rebound in GDP, the unemployment rate has fallen sharpy from its peak of 14.8% in April 2020. Payrolls have picked up in recent months owing to a hiring frenzy among firms as well as the end of enhanced welfare support. The headline measure of unemployment now stands at 4.6%, around 1 percentage point above the level it had been before the pandemic. However, one curious phenomenon has been the lack of the recovery in labour force participation since the summer of last year. Several diverse themes appear to be behind this, but a lack of jobs is not one of them; vacancies are well above their pre‑pandemic levels at more than 10mn. Diminished labour availability has led to a rise in workers’ bargaining power, with the quits rate reaching an all-time high of 3% as a record 4.4mn employees handed in their notice. Pay has had to respond accordingly, with hourly earnings growth running close to 5% on an annual basis.

Inflation should ease back, albeit after climbing higher

On top of this, the US is experiencing a surge in inflation, with the annual rates of CPI and PCE both climbing to respective 30‑year highs. It is a familiar story to other geographies in that it is largely driven by strong demand for durable goods running up against supply bottlenecks. This imbalance should prove temporary, as spending reverts to services and supply chain strains ease.

Source: BLS

Please come and work for us, everybody quit

But the timing of this highly anticipated shift in demand is uncertain, with spending patterns so far proving resistant to return to pre‑pandemic norms. Social activities are amongst the most depressed due to residual COVID‑19 hesitancy and elevated rates of remote working. While we suspect there is a degree of permanency to the latter trend, we would be surprised if there was not a more widespread return to workplaces over time. Nevertheless, for the meantime these supply‑demand imbalances are likely to persist. When coupled with recent pay trends, this should see inflation climb further over the coming months before easing over the latter part of 2022.

Rate hikes to follow the end of QE tapering

Federal Reserve Chair Jerome Powell has remained resolute in his belief that the current bout of inflation is transitory. Under his leadership, the FOMC has begun to rein in its monthly asset purchases, with this ‘tapering’ set to be completed around the middle of next year. Attention has now turned to the timing of ‘lift‑off’ for the fed funds rate. While the FOMC’s inflation objective is likely to be met, it is less clear whether the committee will be satisfied that maximum employment has been attained. It has emphasised this is a “broad-based and inclusive goal” which may not be met if participation rates remain low across certain demographics (e.g. older workers). Given though that this appears to be predominantly voluntary, we expect the fed funds rate to rise gradually after the end of tapering. Consensus expectations on Bloomberg are for the target range to rise 25 basis points to stand at 0.25% to 0.50% by the end of 2022.

A redrawing of the political landscape

Next year’s midterm elections will see at least 34 of the 100 seats in the Senate and all 435 seats in the House of Representatives contested. Currently, the Democrats have an eight‑seat majority in the House and control the 50-50 division in the Senate with the Vice President’s tie‑breaking vote. Generic polls show a narrow lead for the Democrats, but history is not on their side. Since 1934, the president’s party has gained seats in both chambers on just two occasions. It will also be the first election held under the next 10‑year redistricting cycle, for which Republicans control the redrawing of 187 congressional districts, or 2.5 times the Democrats. Depending on the extent to which electoral boundaries are gerrymandered, the GOP may be able to regain the House on this alone. Flipping the Senate is more of a challenge, but betting markets are leaning towards them succeeding. This will mean that the President will become more reliant on bipartisan support for his fiscal agenda, such as the $1tn Infrastructure Bill recently passed.